Sagility

Disrupting or Disrupted?

Sagility

(Disrupting or Disrupted?)

IT service companies minted money, and their market caps grew exponentially since the 1980s. Infosys exemplifies this journey perfectly: Started in 1981 with US$250 capital by 7 engineers in Pune. It took ~18 years to hit $100 million revenue (1999), then exploded:

$1 billion: ~2004

$5 billion: ~2010

~$19–20 billion annual revenue (as of 2026)

(But their business model is now at risk.)

When the tailwinds are in strong favor of a business, management must set the sails right to sail through the business cycle. IT companies just did that.

Based on reports from NASSCOM, government sources, and industry analyses: In recent fiscal years (e.g., FY24 or FY25), the sector contributed around 7–7.5% to India’s GDP. This is massive as IT companies bring in Dollars to manage trade balance. Bringing in US dollars (or earning foreign exchange, primarily in USD) is critically important for India because the country is a major importer of goods like oil, electronics, machinery, defense equipment, and raw materials — most of which are priced and paid for in dollars on the global market.

Key factors behind IT Sector massive growth include:

India’s Economic Liberalization (1991): Global Connectivity.

Offshore/onsite model + cost arbitrage.

Large scalable talent pool.

Global relationships + long term contracts.

Public listings and Capital access.

It is yet to be proven to what extent AI could disrupt traditional IT services business, but one thing is clear that technology is rapidly changing. Today, we look at a business that can be beneficiary of AI, that can integrate artificial intelligence in their business to reduce cost and bring more efficiency.

Let’s look at why Sagility today and how it is different from a Tradition IT services company?

Introduction

Sagility India Limited is a healthcare focused Business Process Management (BPM) / BPO company, basically a specialized outsourcing firm that handles back-office and operational work for the US healthcare industry. It is not a typical IT services company (like Infosys or TCS); instead, it acts like a “behind-the-scenes operations partner” that runs complex, regulated processes for health insurance companies and hospitals/doctors using people, processes, and technology (including AI and automation). Ok, it is also not a software company!

Sounds easy work for them to do but does it really contain moat doing the basic work? Here is what helps Sagility built a business for long term success.

Pure Play Healthcare Focus: (Deep Domain Expertise) - allows intimate knowledge of U.S. healthcare complexities: regulations, reimbursement models, clinical workflows, payment integrity rules, payer-provider dynamics, value-based care shifts.

Tech-Led BPaaS Model (Business Process as a Service) - Not just cost arbitrage — delivers measurable outcomes like reduced denials, faster payments, lower admin costs, better member/provider experiences.

High Client Stickiness & Long-Term Relationships.

Scale + Operational Efficiency in a Growing Market.

Strategic Positioning & Recognition.

Key Services

Claims processing and adjudication.

Revenue cycle management (RCM) for providers (billing, coding, collections, accounts receivable).

Payment integrity and claims cost containment.

Clinical and case management.

Member and provider engagement.

Analytics, utilization management, and population health support.

Other back-office functions like enrollment, credentialing, and data management.

Industry Structure

I have been a life-long fan of businesses that use technology to provide services as it leads to more stickiness, higher switching costs, and more pricing power. It is not easy to disrupt businesses that have the above traits. More likely, the labor cost arbitrage remains as this would be expensive to do the same in the US.

So How is Sagility exhibiting these traits and not subject to disruption?

Stickiness: FY23 and FY24: Retained over 90% of clients.

Average tenure for top clients: 17 years for the five largest client groups.

Things don’t change overnight. I believe the stickiness is here to stay, and Sagility will be able to implement changing AI landscape to bring in more efficiency at reducing costs for clients. Reducing costs for clients? Isn’t that what clients want to hear?

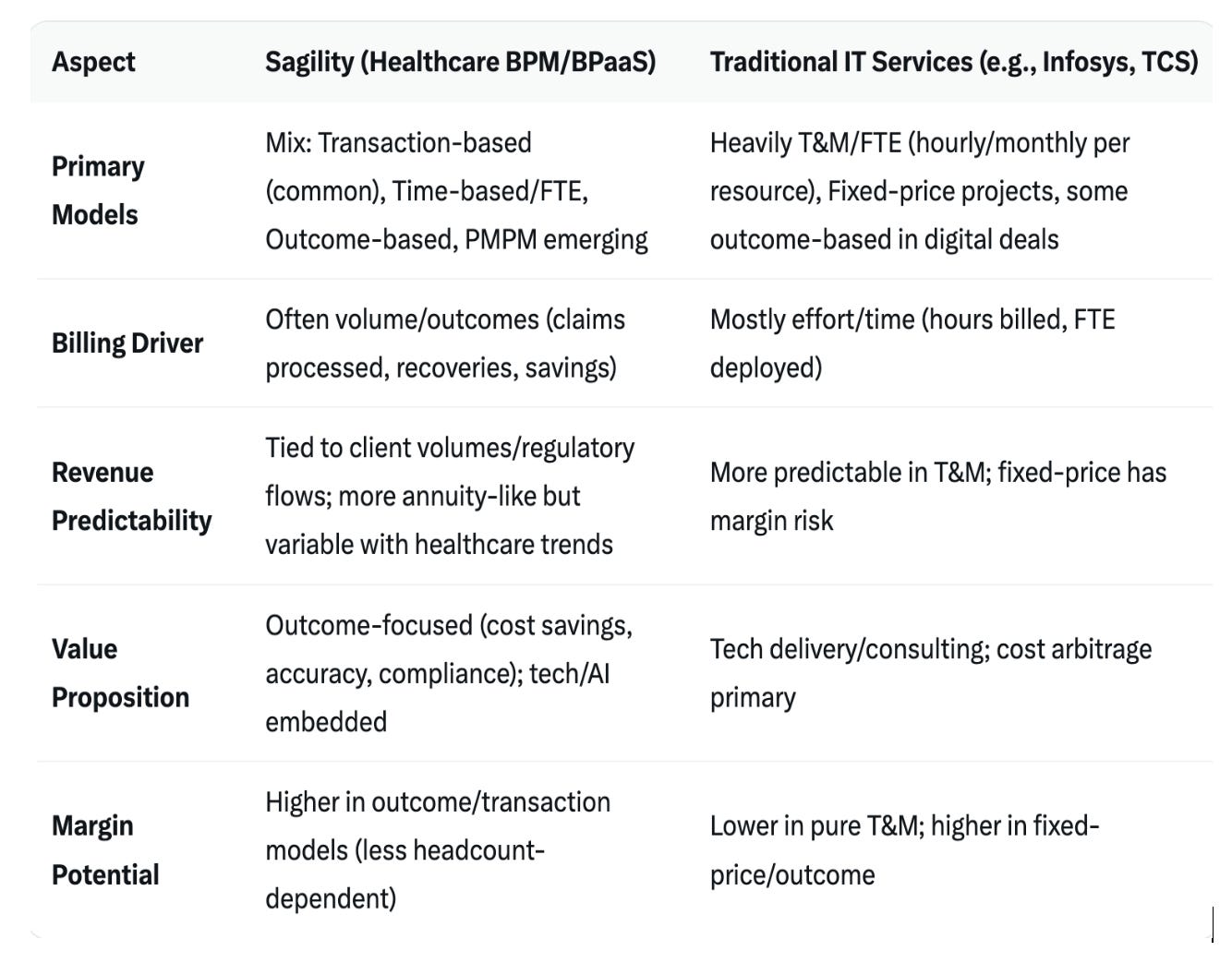

Sagility follows several revenue models and doesn’t risk itself purely from the billable rates model. Sagility does use time-based/FTE-like billing in parts of its portfolio (making it somewhat similar to IT firms), it’s not the core or exclusive model. The company emphasizes transaction- and outcome-based pricing to align with healthcare’s volume-driven, results-oriented nature — this differentiates it from pure IT services, supports stickier revenue, and leverages its domain/tech edge for better economics in a competitive BPO-like space.

Below is the distinguished table for both businesses.

Who are their major clients?

Sagility divides its work into two main client types:

Payers (90% of revenue in recent quarters): These are US health insurance companies (like those offering Medicare Advantage plans, commercial insurance, Medicaid). They pay for medical care and manage claims, members (patients), and providers (doctors/hospitals).

Providers (10% of revenue): Hospitals, physician groups, diagnostic labs, medical device companies, basically anyone delivering care and needing to get paid.

In both the above segments, focus for them would be cost reduction, and Sagility stands to offer the same at healthy margins.

Why Payer is Generally “Better” for Sagility Right Now

Scale and Stability: Payers drive ~90% of revenue, making the business highly dependent on this segment’s performance. Strong payer growth (e.g., 37%+ in 3QYF26) has lifted overall results, raised FY26 guidance (to 22.5%+ constant currency revenue growth), and supported high margins.

Growth Drivers: Payer outsourcing benefits from cost pressures, regulatory complexity, AI/automation (e.g., reducing admin costs), and seasonal boosts like Open Enrollment.

What Services Do They Provide?

For Payers (insurance companies)

They handle the “non-patient-facing” but critical and complicated paperwork, rules, calls, and workflows so doctors/hospitals get paid faster and insurers control costs without mistakes/fraud. For Payers (Insurance Companies):

Claims processing: Checking if a medical bill is valid, approving/rejecting it, paying the right amount.

Member engagement: Call centers for patients (e.g., explaining coverage, enrollment during open enrollment season like AEP for Medicare).

Clinical services: Prior authorization (approving expensive treatments/tests before they happen), utilization management (ensuring care is necessary), case management, appeals.

Provider network operations: Managing doctor lists, credentialing (verifying doctors), and network data.

Payment integrity: Finding overpayments, fraud detection, and recovering money.

Other: Enrollment, billing, contact center support.

For Providers (Hospitals/Doctors):

Checking insurance eligibility before treatment (verifying coverage to avoid surprises).

Medical coding (turning doctor notes and diagnoses into standardized billable codes).

Submitting claims to insurers (electronically filing accurate claims for payment).

Following up on unpaid bills (A/R management — tracking and chasing overdue accounts receivable).

Handling denials/rejections and appeals (investigating why claims were denied and resubmitting corrections).

Patient billing/collections (generating patient statements and managing self-pay collections

They use technology heavily such as AI, machine learning for predicting unpaid claims, automation (RPA), analytics, GenAI for faster work, and platforms like “Sagility Synchrony” for Medicare Advantage.

Understanding business model

The company generates its earnings through three distinct billing structures tailored to the nature of the work performed.

In a time-based model- Clients are charged hourly or monthly rates, which is typically used for specialized services such as clinical care management provided by over two thousand licensed clinicians.

In a transaction-based model - Here they charge a fixed fee per specific task, such as processing a claim or managing a member interaction, which allows Sagility to earn revenue based on the massive volume of work it handles.

Finally, an outcome-based model - ties revenue directly to specific performance results, such as the successful recovery of overpaid claims or the collection of outstanding receivables, aligning the company’s financial success with the cost savings it generates for its clients.

To deliver these services efficiently, the business operates a global multi-shore delivery network with thirty-three centers located in India, the Philippines, Jamaica, Colombia, and the United States. This model combines cost-effective offshore operations for back-office tasks with onshore capabilities in the U.S. for front-office functions that require closer proximity to the client or specific home-based delivery technology.

Furthermore, Sagility is evolving its model by integrating proprietary technology and artificial intelligence, such as its Nurse Assist tool and generative AI solutions, to automate workflows and transition toward a business process as a service model. By Moving into large managed service contracts where they commit to long-term cost takeouts, the company is increasingly becoming a strategic transformation partner rather than a traditional service outsourcer.

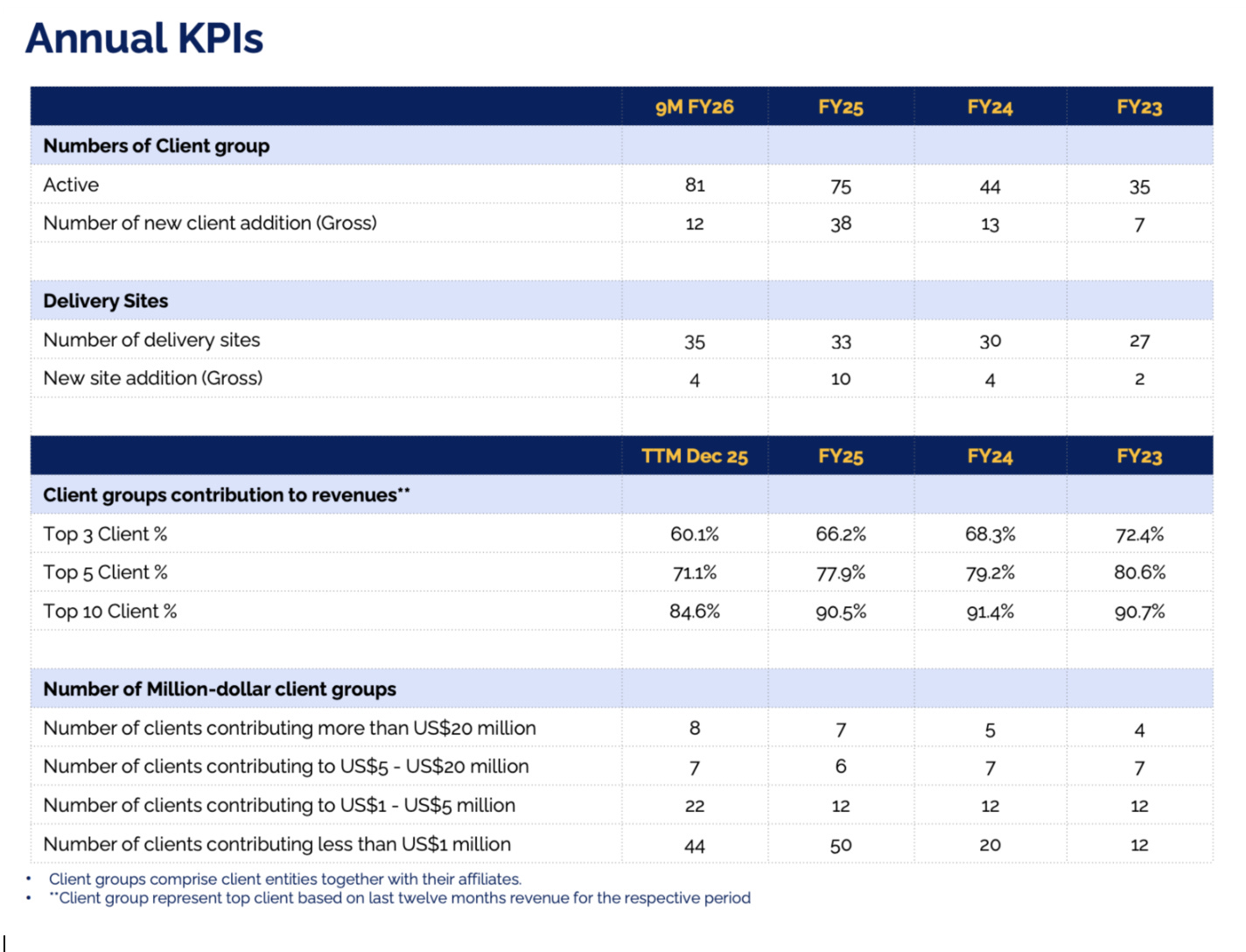

As seen in the above table, improving numbers across all parameters. Top 3 client concentration have reduced to 66.2% from 72.4%. This is expected to go down further over the years as the company adds more clients and scales them. The number of active clients has improved from 35 in FY23 to 75 in FY25. Given the tailwinds from cost reduction and expanding market size, company can continue to penetrate deeper winning market share, increasing client base and reducing concentration to diversify their revenue base.

Clientele information

Top 10 clients contribute 90.5% of revenue. Top 5 clients contribute 78% of revenue, while the top 3 client group alone was responsible for 66% of revenue in FY 2025. These numbers are improving gradually.

Sagility provides services to six of the top ten healthcare payers by enrolment in the United States. Within the U.S. healthcare landscape prominent national carriers include organizations such as UnitedHealthcare, Elevance Health, Centene Corporation, CVS Health, Cigna Healthcare, Humana, Health Care Service Corporation, Highmark, and Kaiser Permanente. The stability of these revenue streams is underscored by the longevity of the company’s partnerships, as the five largest client groups have maintained an average relationship of 18 years with the business. Here revenue concentration risk stays but with the long-term contracts with such US healthcare giants with a good track record shows stability and revenue visibility.

Along with the strong payers network they have diverse group of healthcare providers within the United States, including prominent health systems, large-scale hospitals, and specialized diagnostic centers. Among its notable clients are highly regarded institutions such as Johns Hopkins Hospital, Cleveland Clinic, and Northwestern Memorial Hospital. The company also maintains partnerships with major healthcare networks like Tenet Healthcare, UCSF Health, Cedars-Sinai, and Universal Health Services, as well as specialized providers like Encompass Health.

Sagility has very low exposure to the ACA segment and hence will not be affected by ACA subsidy expiration.

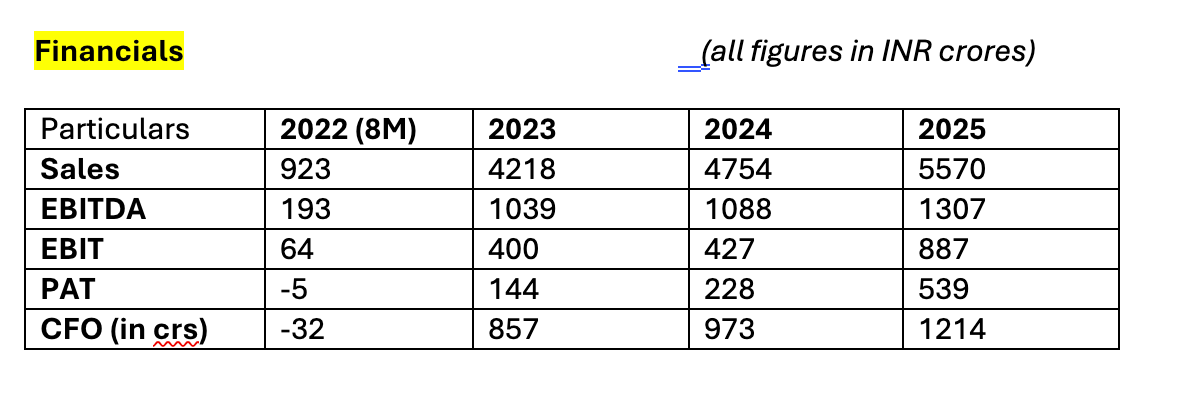

Financial data from 2022 to 2025 shows a significant upward trajectory, but the apparent five-fold jump in revenue between 2022 and 2023 is primarily an accounting artifact. While the 2022 period is legally reported as eight months following incorporation, the company did not acquire its operating business until January 6, 2022, meaning the 923 crore revenue figure captures only about three months of actual commercial activity. By contrast, the 2023 revenue of 4,218 crore represents a full twelve-month operating cycle, making the two periods not directly comparable.

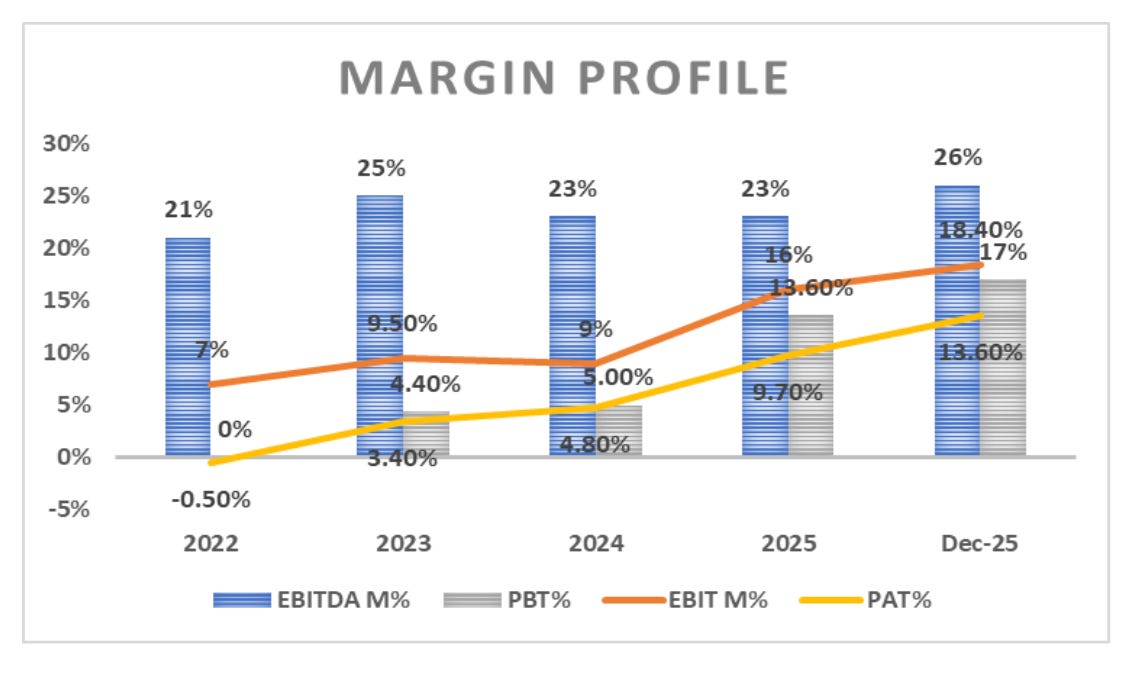

The margin trajectory from 2022 to December 2025 shows consistent expansion across all levels of the profit and loss statement. During this period, the EBITDA margin grew from 21% to 26%, while the net profit margin saw a significant recovery from -0.50% in 2022 to 13.60% by December 2025.

Operational efficiency and offshoring: The company reduced its core employee benefit expenses from 61.6% to 60.8% of revenue by shifting more work to cost-effective offshore locations and improving site utilization.

Reduction in non-cash expenses: Depreciation costs dropped by 32.3% in 2025 because specific intangible assets created during the 2022 business acquisition were fully amortized by the end of the 2024 fiscal year. Basically, depreciation as a % of revenue in 2024 was 14.5% vs 8.4% in 2025, which is the reason for EBIT expansion.

Lower interest costs: Finance expenses decreased from 185 crores in 2024 to 127 crores in 2025 as the company reduced its overall debt through direct repayments and the conversion of promoter debt into equity. Such reasons gave a boost to the company’s profitability margins.

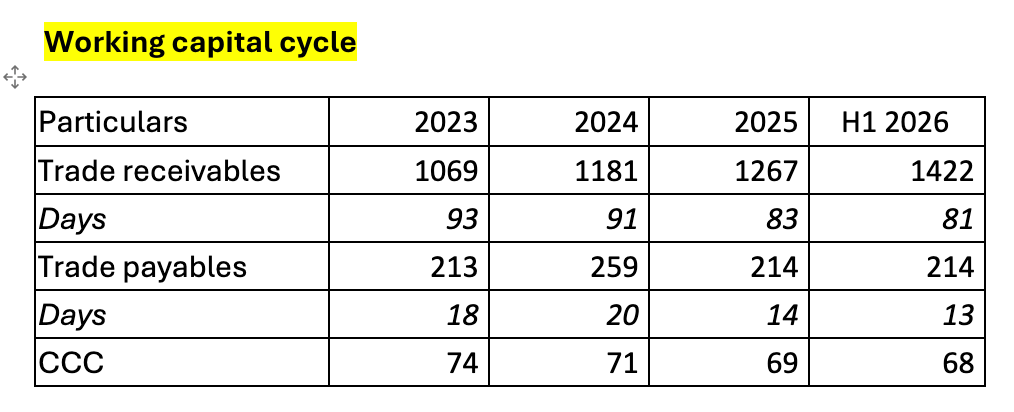

Growth in receivables tracks revenue expansion (FY23 ~₹4,218 crore → FY25 ₹5,570 crore), but DSO has improved overall due to better collections from stable U.S. payer clients and transaction-based models.

Trade payables have hovered in the ₹200–260 crore range in recent years, showing minimal volatility. This is because Sagility’s operations are people-intensive (employee costs dominate) rather than inventory/vendor-heavy, leading to shorter DPO (days payable outstanding) and efficient cash outflows.

Low CCC means quick cash turnover, low WC funding needs, and resilience (funds growth/investments without heavy borrowing).

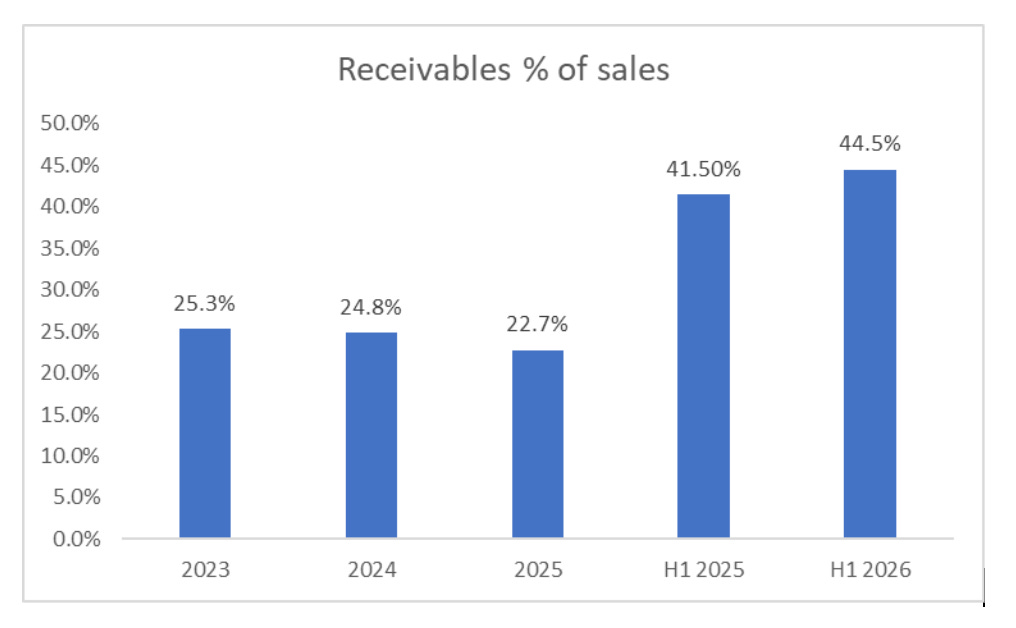

The nature of the business involves significant quarterly seasonality, particularly during the open enrollment period in November and December, which causes revenue to spike in the second half of the fiscal year. Management has noted that during periods of high sequential growth, unbilled receivables tend to rise because a large volume of work is performed but not yet invoiced by the end of the reporting period. For example, in recent quarterly updates, unbilled receivables accounted for 35 days of the total 86-day sales outstanding metric. These unbilled amounts are included in the total trade receivables because the company has an unconditional right to consideration, with only the act of invoicing pending. Consequently, the higher ratios in the half-year data are a combination of comparing a point-in-time balance to a shorter revenue denominator and the temporary build-up of unbilled work during growth phases, which management expects to stabilize once the quarterly revenue growth rate levels off.

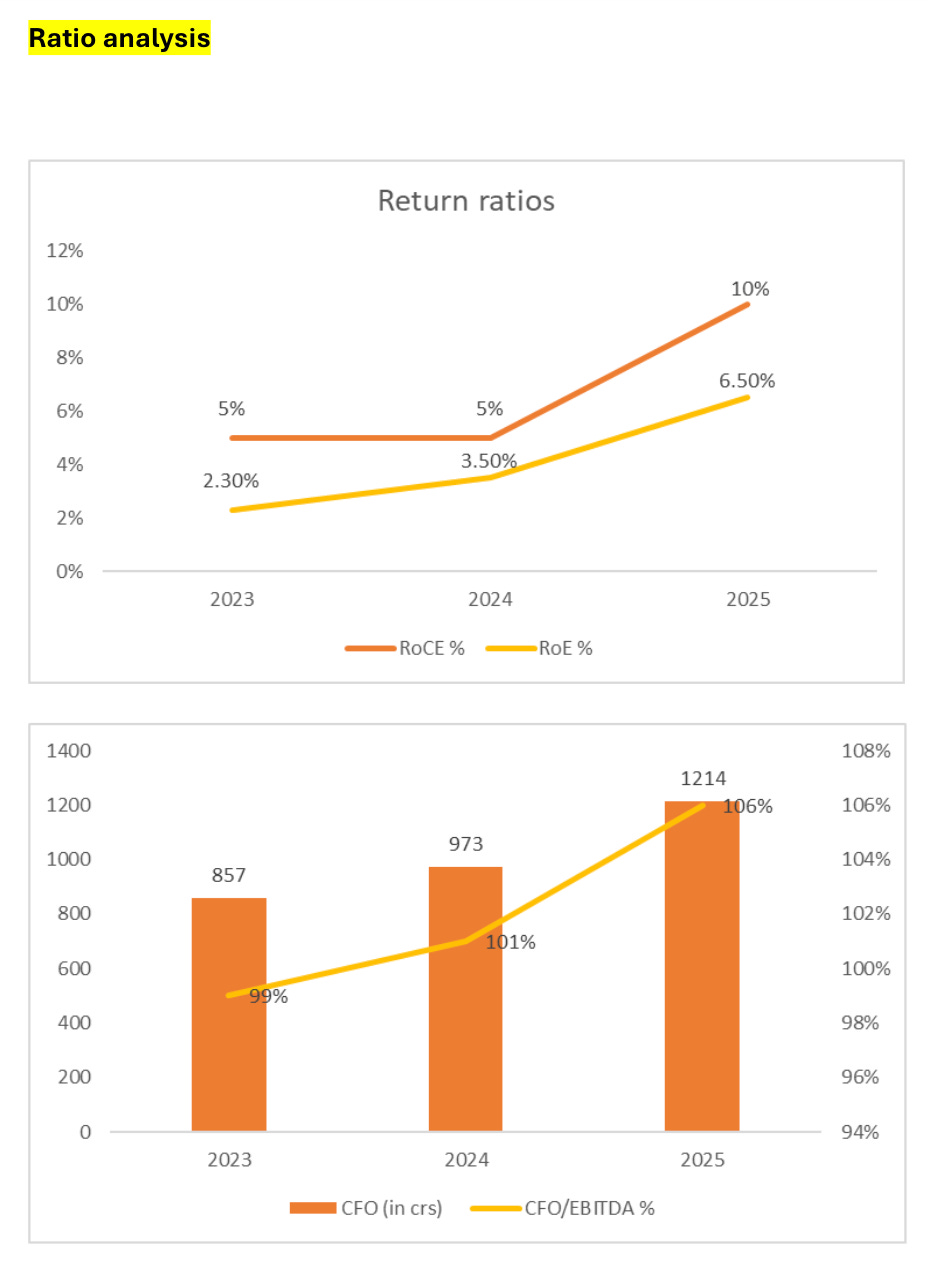

The RoCE shown in the provided data remained steady at 5% during the 2023 and 2024 financial years before doubling to 10% in 2025. This significant improvement in capital efficiency is linked to the sharp rise in profit before tax and the reduction in finance costs as the company scaled its operations. The completion of the amortization cycle for certain intangible assets acquired in early 2022 also removed a significant non-cash burden on earnings, allowing the core profitability of the capital base to be more clearly reflected in the 2025 results.

The RoE followed a consistent upward trajectory, moving from 2.30% in 2023 to 3.50% in 2024 and reaching 6.50% by March 2025. While these reported figures are influenced by a high equity base created by substantial goodwill and intangibles from the initial business carve-out, the trend demonstrates strengthening bottom-line performance. Profit after tax for the most recent year grew by 136% on a consolidated basis, which served as the primary driver for this improved return to shareholders.

A dramatic reduction in the debt-to-equity ratio is evident, falling from 1.2x in 2022 to a very lean 0.17x by the end of 2025. This aggressive deleveraging was achieved through a combination of direct contractual repayments and the strategic conversion of promoter debt into equity. By allotting 394 million new equity shares to its promoter for consideration other than cash, the company successfully expanded its equity base while simultaneously extinguishing large interest-bearing liabilities.

These trends collectively signify a major strengthening of the company’s financial fundamentals and overall balance sheet resilience. The rapid reduction in debt has significantly lowered interest expenses, which directly boosts net profit margins and provides the financial flexibility to fund future organic growth

nd selective acquisitions through internal accruals. Furthermore, the strong cash conversion and rising returns suggest that the company is entering a phase of mature, self-sustaining operations where it can efficiently generate value from its assets while maintaining a very conservative leverage profile.

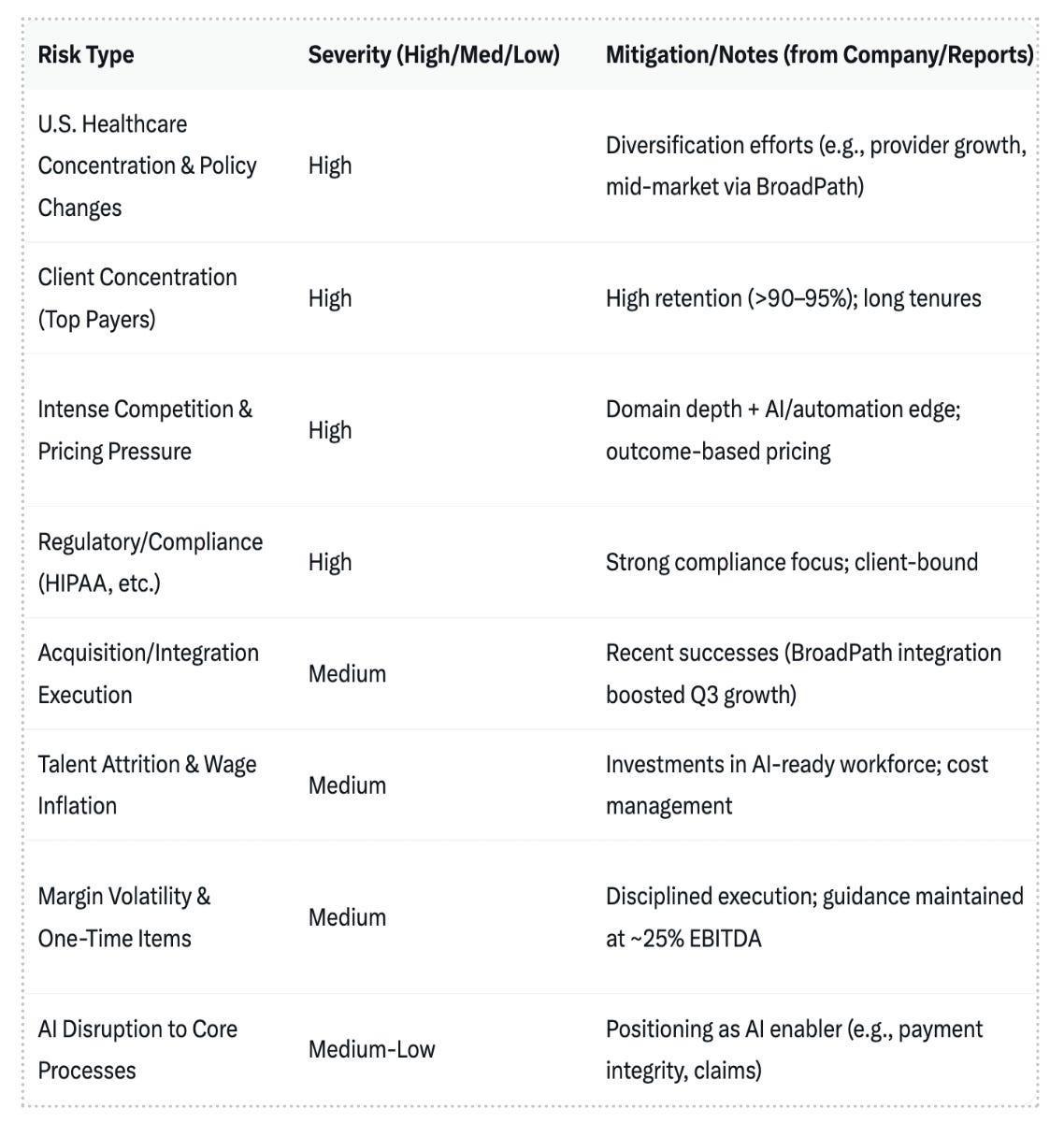

Risks:

Client concentration: Top 10 clients contribute 90.5% of revenue. Losing a single client can impact the company more widely.

Regulatory and Policy Risks:

Heavy exposure to U.S. healthcare regulations.

Compliance failures (data privacy, security breaches) pose reputational/financial risks in a highly regulated space.

Competitive and Market Risks:

New entrants with innovative/AI models could pressure pricing/margins.

Shift to in-house operations or reduced outsourcing adoption (e.g., due to cost pressures or data privacy concerns).

Threat from AI

If AI commoditizes routine processes, clients (payers/providers) may demand lower rates or outcome-based contracts with steeper savings guarantees.

Many of Sagility’s high-volume services — like claims intake/review, error detection, simple adjudication, appeals drafting, denials reversal, and basic RCM workflows — are rule-based or pattern-driven. GenAI and agentic AI (autonomous agents) can handle these faster/cheaper with minimal human intervention.

Why AI Threats May Be Overstated for Sagility

Healthcare Complexity Shields Against Full Automation: Sagility’s hybrid model (AI + domain experts) adds value.

AI as Growth Enabler, Not Destroyer.

Regulatory Barriers Slow Disruption.

Client Stickiness and Diversification.

Valuations:

Stock is attractively priced at 21x P/E. Company has raised revenue guidance for 22.5% top line growth from previous guidance of 21%. With guided 25% stable operating margin and conservative 20% growth in EPS, stock is currently trading at 15x forward P/E multiple. P/E multiple will further compress in FY27 as company plans to be debt free. This should help grow the bottom line faster.

Company earned 0.57 per share in 3QFY26. If i annualize this, it comes to 2.28 for the year and with 20% growth, expect company to do 2.736 EPS in FY27. This is giving me a forward multiple of 14.47. Stock is attractively priced.

The company also generated 1,214 cr in operating cash. At today’s market cap of 18,500 cr, stock is trading at 15x Operating cash.

Disclaimer: The stock mentioned is not an investment recommendation. This information is solely for educational purpose only. I write on companies listed in the Indian and the US stock market. For BUY/SELL recommendation, kindly reach out to your financial advisor.